Market Update - Month Overview (February 2025)

Summarised by Shara Cox (Report via Zenith)

International Market Summary

Global equities experienced a mixed performance in February 2025. European stocks led gains, rising 3.7%, supported by improved growth prospects, ECB policy easing, and geopolitical developments. In contrast, US equities declined by 1.6% as economic data weakened, with declining consumer confidence, lower retail sales, and softening GDP growth projections. The Federal Reserve kept interest rates at 4.25%-4.5%, but market expectations shifted toward three potential rate cuts over the next year. The US dollar showed weakness amid trade policy uncertainty, as new tariffs were announced against Canada, Mexico, and China. Emerging markets saw volatility, with China’s equity market surging 11.8% on growth stabilization and AI-driven optimism, while Indian and Korean markets struggled. Global fixed income performed well, as bond yields fell amid expectations of softer economic growth. Commodities saw mixed movements, with gold nearing record highs due to geopolitical risks and inflation concerns, while oil declined over 5% on potential conflict resolution in Ukraine.

Australian Market Summary

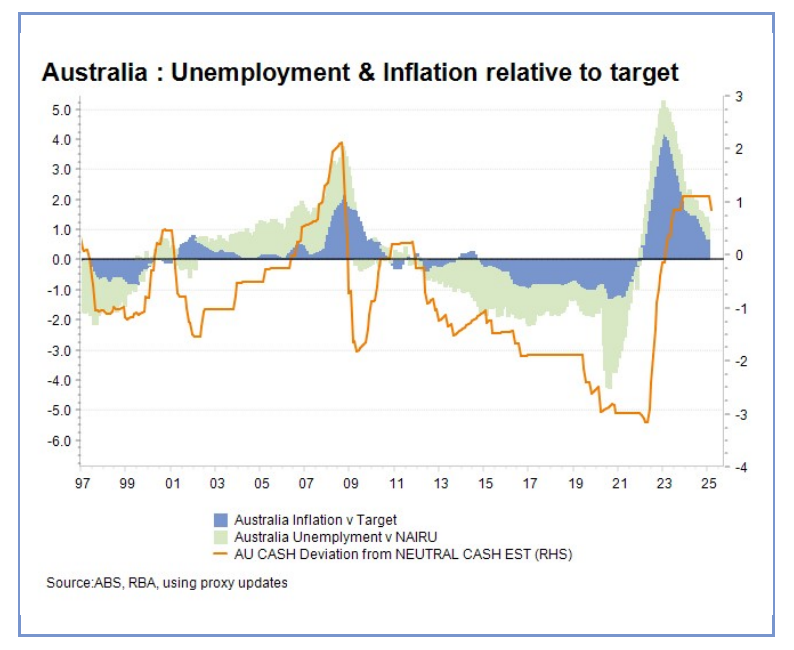

The Australian equity market continued its underperformance relative to global peers, falling 3.8% in February. The ASX 200 initially reached record highs above 8500, buoyed by expectations of an interest rate cut from the Reserve Bank of Australia (RBA). However, the market reversed its gains following the widely anticipated rate reduction to 4.1% on February 17, as concerns over global economic uncertainty, weaker US data, and tariff tensions weighed on sentiment. Despite the pullback, Australian equities have gained 9.9% over the past year. The financial sector was hit hard, with bank stocks declining 4.6%, despite remaining up nearly 26% over the past year. Other sectors such as healthcare (-7.6%), IT (-12.3%), and REITs (-6.3%) also faced sharp declines, while food and beverage stocks emerged as the only notable outperformers, rising 7.8%.

On the economic front, data remained relatively strong, with retail sales volumes seeing their best quarterly rise since 2022 and the labour market continuing to show resilience. Employment grew by 44,000 in January, pushing annual job growth to 3.5%, while the unemployment rate remained low at 4.1%. Despite tight labour market conditions, the RBA expects core inflation to ease to 2.7% by mid-year, supporting market expectations for a shallow easing cycle, with the cash rate projected to settle around 3.5%.

Australia has largely been insulated from the immediate impact of Trump’s new tariffs, though risks remain, particularly regarding trade relations with China. A potential escalation in the US-China trade war could negatively affect Australian exports and investor confidence.

Meanwhile, the Australian dollar fluctuated, briefly rising above 64 US cents before falling back to 62 cents as risk appetite diminished. In fixed income, bond markets responded favourably to the RBA’s rate cut, with Australian government bond yields declining. Commodities saw mixed movements, with iron ore and copper prices strengthening, while gold surged towards the US$3000 mark amid global geopolitical uncertainty. Looking ahead, Australian markets remain sensitive to global economic shifts, particularly US and Chinese growth trends, central bank policies, and evolving trade dynamics.