Market Update - Month Overview (March 2025)

Summarised by Shara Cox (Report via Zenith)

International Market Summary

In March 2025, global equity markets delivered strong performance, led by a rally in US stocks. The MSCI World Index (hedged to AUD) rose by 3.4% for the month. US equities were a key driver, with the S&P 500 advancing 3.1%, buoyed by a more dovish tone from the US Federal Reserve, continued signs of easing inflation, and robust earnings from the technology sector. The Fed kept its benchmark interest rate unchanged at 5.25–5.50%, but investor sentiment was lifted by growing expectations of potential rate cuts later in the year as inflation moderates further.

European markets mirrored the positive momentum in the US, as inflation appeared to stabilise and investors began to anticipate a shift toward looser monetary policy. The Euro Stoxx 50 index climbed 4.3% over the month. In Asia, Chinese equities also gained ground, with the Shanghai Composite up 1.2%, helped by government policy support and tentative signs of economic stabilisation. Japan’s Nikkei 225 rose 2.6%, benefiting from a weaker yen and strong corporate earnings. Across global bond markets, yields declined in both the US and Europe, reflecting expectations of future rate reductions and a more accommodating policy stance from central banks.

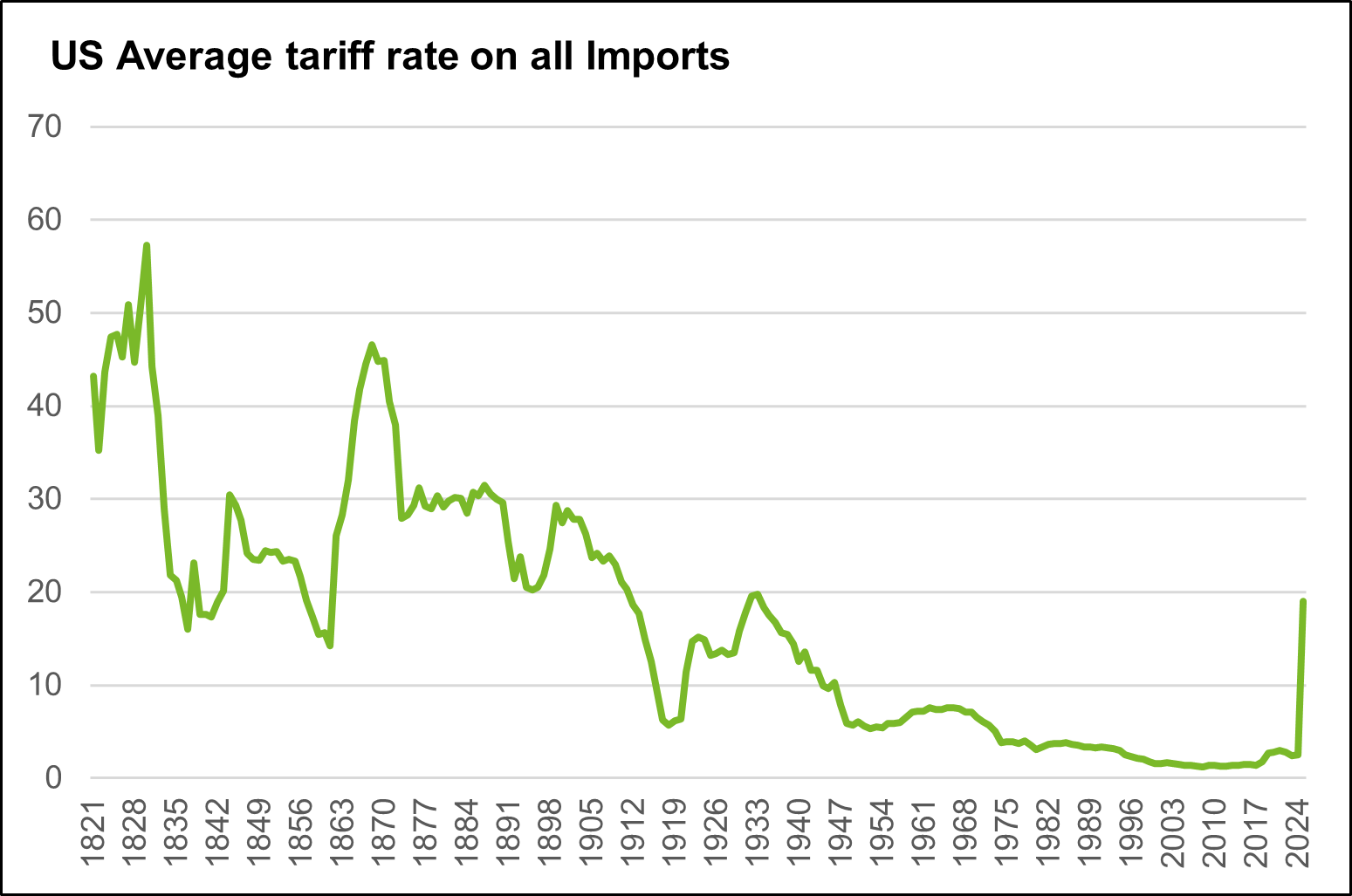

However, geopolitical developments began to cast a shadow over this positive sentiment. The saga of Trump’s tariffs intensified in March, culminating in the announcement of sweeping tariffs on most US trading partners in early April. A minimum base tariff of 10.0% was applied across the board, directly affecting Australian exports to the US. Tensions with China escalated further, with the implied US tariff on Chinese goods reaching 67.0%, including a 34.0% reciprocated tariff layered on top of existing levies. While markets remained resilient during March, these trade developments have introduced a layer of uncertainty heading into the second quarter, with investors now closely watching how global trade dynamics could affect inflation, supply chains, and central bank policy.

Australian Market Summary

Australian equity markets had a solid month in March, with the ASX 200 rising by 3.5%. The recovery was broad-based, with notable strength in the technology, financial, and materials sectors. This rebound followed earlier softness and was supported by improving global sentiment and relatively stable domestic economic conditions.

The Reserve Bank of Australia (RBA) left the official cash rate unchanged at 4.35%, as inflation, while still above target, showed signs of easing. The decision to hold rates was widely anticipated, and markets remain focused on the RBA’s future policy direction, which will largely depend on the trajectory of inflation and domestic demand. On the economic front, unemployment edged slightly higher but remained historically low, suggesting continued resilience in the labour market. Retail spending was flat for the month, pointing to cautious consumer behaviour amid persistent cost-of-living pressures. Australian bond yields followed global trends lower, as expectations solidified around a steady interest rate environment in the short term.

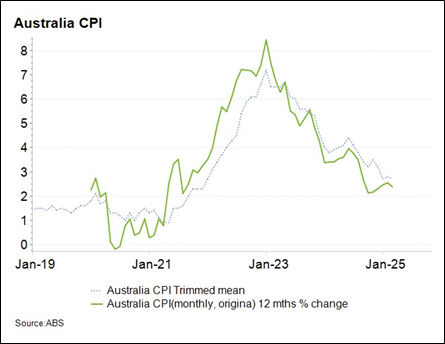

March also brought some positive news on the inflation front, with February CPI data revealing a drop in core inflation to 2.7%, placing it within the RBA’s target range of 2–3%. This moderation has supported expectations that the RBA could move toward easing later in the year if the trend continues. Meanwhile, the Australian housing market showed tentative signs of a rebound, with house prices posting modest gains over the quarter, supported in part by the February rate cut. These developments suggest that while consumers remain cautious, lower inflation and stabilising rates are beginning to provide a more constructive backdrop for housing and broader economic sentiment.