Market Update - Month Overview (May 2026)

Summarised by Shara Cox (Report via Zenith)

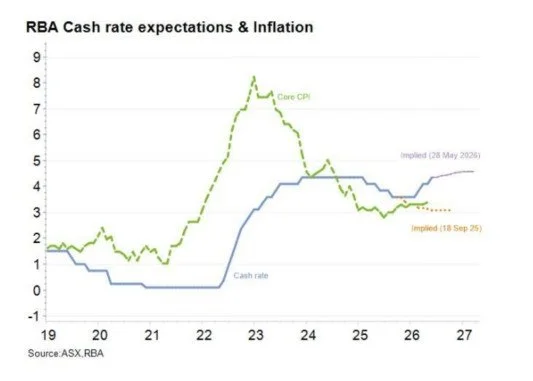

Australian Market Summary

Australian markets delivered more modest gains and lagged global peers, reflecting a combination of tighter monetary policy and a softer domestic economic backdrop. The Reserve Bank of Australia increased the cash rate to 4.35% in May, maintaining pressure on households and businesses as inflation concerns persist. Although headline inflation has begun to moderate, core inflation remains elevated, reinforcing the cautious policy stance. At the same time, economic indicators weakened, with rising unemployment and declining consumer and business confidence weighing on sentiment.

Equity market performance was mixed, with strength in materials supported by commodity prices, but weaker outcomes across financials and healthcare sectors. The local market’s relatively low exposure to high-growth technology sectors also contributed to underperformance compared to international indices. On a more positive note, Australian bond markets strengthened toward the end of the month as expectations for further rate hikes eased. The Australian dollar was supported by higher interest rates and firm commodity demand, although ongoing concerns around domestic growth and China’s outlook limited its upside.

Image Sourced from Zenith

International Markets:

Global markets continued their strong upward trajectory in May, supported by resilient corporate earnings and sustained investor enthusiasm for AI-driven growth themes. Technology and semiconductor companies were the clear leaders, benefiting from ongoing demand for data infrastructure and digital capabilities. This trend was particularly evident in the US, where earnings growth remained robust, reinforcing confidence in global equity markets. Emerging markets also outperformed, driven largely by Korea and Taiwan, where semiconductor production linked to AI continues to underpin strong returns.

While equity markets advanced, bond markets experienced some volatility during the month. Yields initially rose amid lingering inflation concerns, before easing later as oil prices declined and economic data softened. This helped stabilise fixed income markets and improve overall investor sentiment toward month-end. Meanwhile, geopolitical risks in the Middle East had a limited lasting impact, with easing energy prices helping to reduce inflation pressures and support global market stability.