Oil Shocks & Central Bank Responses

Report from Zentih, summarised by Steve Landers

Geopolitical tensions and the sharp rise in oil prices following the US–Israel conflict with Iran have revived a key market question: could a sustained rise in energy prices threaten the global economic expansion? Historically, oil spikes have been inflationary, often prompting tighter monetary policy and periods of equity market volatility.

The US likely did not foresee the near-closure of the Strait of Hormuz, through which approximately 20% of global oil and LNG supplies transit. Iran's effective closure of the waterway has materially altered the supply picture:

• An estimated 4.5–5 million barrels per day (approximately 5% of global supply) have been lost since the conflict began, with that figure projected to potentially double by mid-April as the physical lag in shipping works through.

• Refineries and LNG facilities in Bahrain, Kuwait, Qatar, Saudi Arabia, and the UAE have been targeted by drone and missile attacks. Qatar declared force majeure on LNG exports — Qatar supplies approximately 20% of global LNG.

• Saudi Arabia and Iraq have been forced to cut production due to lack of storage capacity. Analysts warn that even if the strait reopens, infrastructure damage could delay a return to normal supply levels.

Yemen's Houthis have opened a new front by firing ballistic missiles at Israel and threatening the Bab el-Mandeb Strait — another critical shipping chokepoint carrying an estimated 4–5 million barrels per day. Analysts at Societe Generale warn that disruption there could push prices as high as US$150/barrel in April.

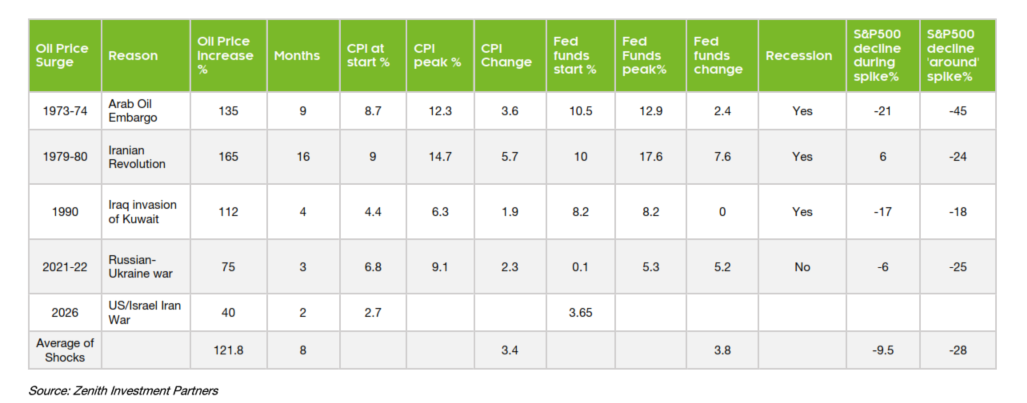

A Brief Look at History

Past supply-driven oil shocks typically lifted CPI by 2–5 percentage points, as higher fuel and transport costs flowed quickly through the economy. Central banks, most notably the US Federal Reserve, have generally responded with significant tightening, with policy rates rising by an average of almost 4 percentage points during oil supply shock periods.

Recessions have followed many of these episodes, and equity markets have tended to struggle, with the S&P 500 typically falling around 10% during the spike and 25–30% around the full adjustment.

What Is Different Today

While the recent rise in oil prices is significant, it remains far below the levels observed during the most severe previous recessionary periods. The global economy has also become less energy-intensive over time. Each sustained US$10 increase in oil prices is expected to add approximately 0.3–0.4 percentage points to US inflation. In Australia, the same magnitude of price increase translates to about 10 cents per litre at the pump, feeding quickly into household budgets and sentiment.

Outlook

The longer global oil supply remains constrained, the higher the probability that elevated prices feed more broadly into inflation, policy tightening, and growth expectations. The ongoing negotiations between Washington and Tehran mean market volatility is likely to persist.

The scale and duration of the supply shock is now more consistent with the 1973–74 and 1979–80 episodes than initially anticipated — both of which resulted in recessions. The 2026 shock differs in that the global economy entered the event with lower inflation and higher interest rates than in prior episodes, providing some offset.

The resolution pathway remains highly uncertain. A rapid diplomatic breakthrough could deliver sharp market relief. However, the physical damage to Gulf energy infrastructure means a normalisation of oil supply could take weeks to months even post-ceasefire.

Our Response

Salt and our Investment Consultant, Zenith, continues to closely monitor developments in the Middle East and their implications for global growth and inflation. Thus far, underlying economic fundamentals remain solid, though the inflation outlook has clearly deteriorated. In this environment, we wish to remain invested in the market and look for pricing opportunities.