Salary Packaging an Electric Vehicle: Why Timing Matters After the Federal Budget

Written by Daniel Dubois

With fuel prices remaining elevated following ongoing global oil supply disruptions, electric vehicles (EVs) continue to attract attention from employees looking to reduce running costs and improve tax efficiency. Salary packaging an eligible EV through a novated lease remains one of the most tax effective vehicle strategies currently available. The 2026–27 Federal Budget announcements on Tuesday have now proposed significant changes to the existing Fringe Benefits Tax (FBT) concessions.

While the current rules remain in place for now, the Budget announcements mean employees and employers considering an EV arrangement may wish to review their options sooner rather than later.

What is salary packaging an electric vehicle?

Salary packaging (or salary sacrifice) allows employees to pay certain expenses from pre-tax income, reducing taxable salary. When applied to vehicles, this is generally done through a novated lease, where lease repayments and running costs are deducted directly from gross salary. Normally this attracts Fringe Benefits Tax (FBT) which uses various calculation formula to effectively tax the personal component of this benefit at 47%.

Under the current rules, eligible electric vehicles receive an exemption from FBT, significantly improving the after-tax cost compared with traditional petrol or diesel vehicles. You can effectively receive a full tax deduction for the purchase and financing of the vehicle across the life the novated lease.

The current FBT exemption

Ordinarily, employer-provided vehicles are subject to FBT. However, eligible electric vehicles are currently exempt, creating substantial tax savings for employees using novated lease arrangements.

To currently qualify, the vehicle must be:

a battery electric or hydrogen fuel cell vehicle

plug-in hybrid vehicles generally no longer qualify from 1 April 2025 unless grandfathered under older arrangements,

first held and used on or after 1 July 2022,

below the luxury car tax threshold

for 2025-26, the EV threshold is $91,387,

designed to carry under one tonne and fewer than nine passengers, and

provided to a current employee.

Federal Budget changes - proposed reduction in EV concessions

The 2026-27 Federal Budget proposes scaling back the current EV FBT exemption over coming years.

Under the proposed rules:

From 1 April 2027:

full exemptions would only apply to EVs valued below $75,000,

EVs above $75,000 but below the luxury car tax threshold would receive only a partial exemption.

From 1 April 2029:

all eligible EVs below the threshold would receive only a 25% exemption rather than a full exemption.

Importantly, these measures are not yet law and still require passage through Parliament. However, they indicate a clear shift away from the generous concessions currently available.

For employees considering a novated lease arrangement, acting before these changes commence will preserve access to the more favourable rules currently in place.

What costs can be packaged?

Eligible EV arrangements can typically include:

lease repayments,

registration,

insurance,

servicing and tyres, and

electricity used to charge the vehicle.

Where charging occurs at home, the ATO currently allows simplified methods for calculating electricity costs, reducing record keeping requirements.

How does this save tax?

Savings arise because:

vehicle costs are paid from pre-tax income;

eligible EVs currently avoid FBT;

GST is incorporated into the arrangement; and

EV running costs are generally lower than petrol or diesel vehicles.

For employees on moderate to higher marginal tax rates, the overall benefit can still amount to thousands of dollars per year under the current rules.

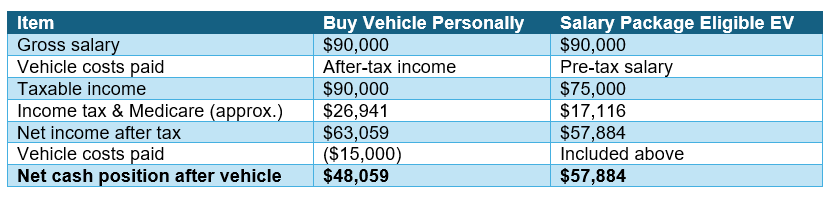

Worked example - $90,000 salary: buy privately vs salary package an eligible EV

Assumptions:

Gross salary $90,000

Resident individual, no other deductions or offsets

Medicare levy of 2% applies

Eligible battery electric vehicle currently fully FBT exempt

Annual vehicle cost (lease + running costs) $15,000

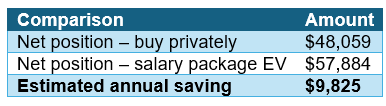

Estimated annual benefit of salary packaging

The benefit may be even greater for higher income earners due to higher marginal tax rates.

An important consideration – reportable fringe benefits

Although eligible EVs may currently be exempt from FBT, the benefit may still appear as a reportable fringe benefit amount on an employee’s income statement.

While this does not increase income tax directly, it can impact:

HELP repayments,

Medicare levy surcharge,

private health insurance rebates, and

other income-tested entitlements or obligations

Final thoughts

Despite the proposed Budget changes, salary packaging an eligible electric vehicle remains one of the most tax effective vehicle strategies currently available for many employees.

The Government’s proposed scaling back of EV FBT concessions mean timing will become increasingly important. Employees considering taking up a novated lease arrangement - particularly for higher value vehicles - may benefit from reviewing their options before the proposed changes commence from April 2027.

As always, eligibility rules and personal circumstances matter, and professional advice should be obtained before entering into any arrangement.

If you are considering salary packaging an electric vehicle for yourself, or offering EV novated leasing through your business, please contact your Salt Adviser so we can assist with reviewing the tax and cash flow implications under both the current and proposed rules.