GENUINE REDUNDANCY PAYMENT: AGE INCREASE

The qualifying age to receive a genuine redundancy payment has recently been increased to the age pension age, so even if you’re over 65 you may still be able to receive the payment. The advantage of that is you’ll potentially be able to work longer and retire later in life whilst still being able to receive a tax-free genuine redundancy payment. However, the rules surrounding this area is quite complex and is largely dependent on the facts of each case, so caution is advised.

With everyone retiring later in life and working longer, the government has been playing catch up to align some outdated age provisions in the tax law to today’s standards. One such change brings into line the genuine redundancy payment’s qualifying age with the age pension age. In real world terms, it means the qualifying age has been increased from 65 to between 66 or 67 depending on the year you were born. So, if you’re dismissed on or after 1 July 2019, and are between 65 and 67, you may potentially qualify for more of your redundancy payment to be tax-free depending certain eligibility conditions.

Read More

OCTOBER REPORT

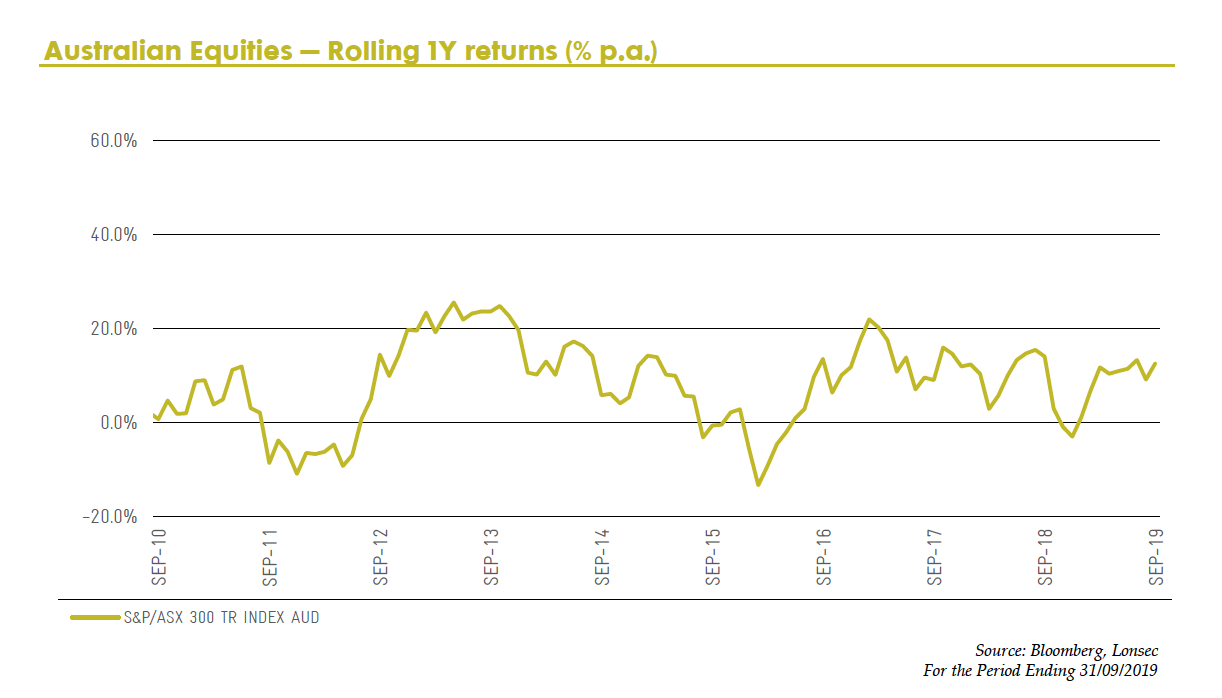

Australian shares managed to reclaim some ground in September which saw the S&P/ASX 200 Index post a modest 1.8% return before falling in the first week of October. Energy was the top performing sector, returning 4.7% and clawing back some losses from the previous month. Oil price spiked in September, the result of major disruption to the oil market, which favoured energy producers like Santos (+7.2%) and Beach Energy (+3.3%). The financial services sector (+4.1%) saw broad growth over the month. Shares in IOOF (+26.0%) rose as the wealth manager completed its sale of Ord Minnett during the month and the Federal Court dismissed a case brought against it by APRA that accused executives of failing to act in its members’ interests.

Read More

SELLING SHARES: HOW DOES TAX APPLY?

Did you know that when you sell your shares, the size of your capital gains tax bill is affected by how long you’ve held the shares, and how you offset your capital gains and losses? Knowing the tax rules can help you plan ahead. Whether you own just a few listed shares or have an extensive portfolio, understanding how capital gains tax (CGT) applies when you sell your shares can help you plan your trades effectively. Here, we break down the rules for taxpayers who hold their shares as a passive investment. If you trade shares on a scale that amounts to a business of share trading, talk to your tax adviser about the different tax regime that applies. Each time you sell a parcel of shares, you trigger a “CGT event” and you must work out whether you’ve made a capital gain on that parcel (where the proceeds you receive exceed the cost base) or capital loss (where the cost base exceeds the proceeds). You also trigger a CGT event if you give the shares away as a gift – perhaps to a family member. For tax purposes, you’re deemed to have disposed of the shares at their full market value.

Read More

CLOSING THE TAX GAP: ATO FOCUS ON INDIVIDUAL RETURNS

The ATO will scrutinise every individual tax return lodged for the 2018-19 income year to find instances of incorrect claims. It is encouraging taxpayers to document supporting evidence for all claims as it seeks to recoup $8.7bn in lost tax revenue each year from small over-claims by a large proportion of taxpayers. Red flags which may lead to ATO contact or audit include under reported income (from third party data) and deductions that appear high compared to others with a similar job and income level.

As this year’s tax time comes to a close, the ATO has warned that it will scrutinise every individual tax return lodged to seek out incorrect claims. In particular, it will be on the lookout for under reported income as indicated by third party data, and deductions that appear high compared to people with a similar job and income level.

Read More

RETIREES AND THE COMMONWEALTH SENIORS HEALTH CARD

In our article, ‘Ageing and health status in retirement: The three chapters’, we discussed the different chapters that you will experience as you make your way through life.

For example: 1. the accumulation chapter,2. the transition to retirement chapter (where applicable), and3. the retirement. From a retiree’s perspective, the retirement chapter can be broken down even further. For example: 3a. the early (active) chapter, 3b. the middle (passive/sedentary) chapter, and 3c. the late (frail/support) chapter. The defining features of each chapter are evident. Particularly so, when you look at them in comparison to each other over several key areas. For example, in terms of finances, when your age starts to get the better of your health, you will most likely find that your healthcare expenditure increases. With this in mind, we take a closer look at the Commonwealth Seniors Health Card.

Read More

REVERSE MORTGAGES: THE PENSION LOANS SCHEME

Retirement should be a chapter in your life when you can finally kick back and enjoy the fruits of your labour. Leading up to this point, you worked hard to not only pay down debt, but also accumulate sufficient wealth to generate income to self-fund the retirement lifestyle that you envisioned for yourself.

However, for one reason or another (e.g. financial hardship, unforeseen circumstances, or even failure to plan), some find themselves entering, or ending up in, retirement ‘asset-rich, but income-poor’– with the majority of their wealth tied up in the family home (i.e. an asset that doesn’t typically generate income).

Read More

ATO FOCUSING ON INVESTMENT STRATEGY DIVERSIFICATION REQUIREMENTS – WHAT DO TRUSTEES AND AUDITORS NEED TO DO?

The ATO recently identified approximately 18,000 SMSFs who hold 90% or more of their assets in a single asset or a single asset class. The ATO is concerned that these funds may not have met their investment strategy requirements and has reminded trustees that failure to do so can result in an administrative penalty of $4,200. So, what do these trustees and their auditor need to do to avoid penalties being applied?

The superannuation law requires all SMSF trustees to “formulate, regularly review and give effect to” an investment strategy for the fund.

Read More

1 APRIL 2020: 'PROTECTING YOUR SUPER PACKAGE' 2.0

In our article, ‘Legislative update (Bills): To be, or not to be… (Part 1)’, we discussed the fact that a number of Bills lapsed due to the dissolution of parliament ahead of the 2019 federal election.

Furthermore, when parliament resumed post-election, if the desire remained to proceed with these Bills, then they would need to be introduced as new Bills and make their way through the parliamentary process.

With this in mind, the Treasury Laws Amendment (Putting Members’ Interests First) Bill 2019 was introduced on 4 July 2019 and received royal assent on 2 October 2019.

Read More

THE TOP 10 FACTS ABOUT ACCOUNT BASED INCOME STREAMS

As retirement moves closer into focus, you might start to give a thought towards the options available to you. Especially, in terms of utilising the accumulated wealth inside of super, to fund your retirement lifestyle.

It’s important to understand that there are several options available to you; for example, depending on your personal circumstances, you can choose to take your super benefits as: a lump sum, an income stream, or a combination of both. Briefly, those that choose to take their super benefits as a lump sum, can often do so for one or a combination of reasons.

Read More